… and why you won’t get your loan back (probably).

Venture-stage companies are fundamentally risky. It’s tempting for the investor, looking for ways to reduce their risk and improve their returns, to invest a loan rather than share capital. This post explores how that approach can lead to both commercial and tax problems further down the line.

How a loan structure might increase your portfolio return

A quick note upfront: we’re not talking here about ASAs (Advanced Subscription Agreements) which are essentially equity instruments and, crucially, treated as such for tax purposes - see our earlier post.

The basic idea of using loan instruments to make a venture investment is a simple one and makes good sense. The idea is that, instead of 100% of the investor’s cash going into the company as equity, the bulk is invested as a repayable loan, and only a sliver as equity. Much like a private equity structure. That way the investor gets to have their cake and eat it – the risk capital comes back out and they get to share in the upside as well.

Take our usual example of SaaSco funding offer of £1m for 20% of the company. Wouldn’t it be better for the investor to have put in, say, £900k as a loan, and just £100k of equity for their 20% stake? These are the positives:

- Bigger returns: the obvious advantage is getting an extra £900k on a successful exit, in addition to the value of the equity stake (although note: the investor’s gain is pound-for-pound a cost to the founders and other shareholders – a chunk of prior capital accruing at 12% in a start-up is real disincentive to management if things aren’t going to plan);

- Quicker returns: if SaaSco manages to redeem the loan before the company as a whole exits (which might be years into the future) then the investor gets most of their monies back early and can either recycle their capital into new ventures or simply enjoy being de-risked. Either way, their portfolio returns are enhanced;

- Downside protection: if SaaSco hits hard times, the loan ranks ahead of share capital. The investor therefore has more chance of recovering some of their investment if they hold a loan rather than pure equity.

- Negotiating position: alternatively, if SaaSco struggles, the investor has the option to negotiate to convert the loan into equity, increasing their stake to mitigate SaaSco’s diminished value.

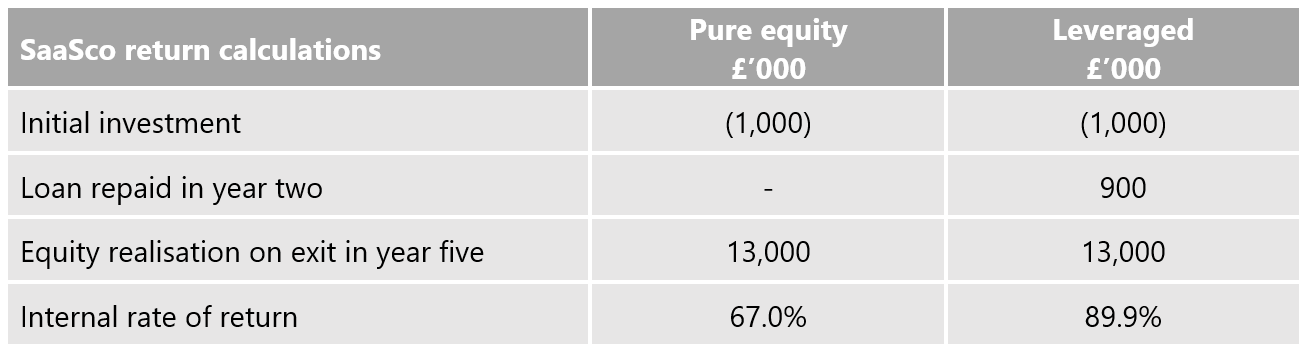

Let’s examine what the enhanced return might look like for SaaSco. Remember, we were planning to invest £1m, and in our previous posts we’ve assumed that after five years the equity stake might be worth £13m. In the leveraged scenario, let’s assume that the investor manages to get their £900k loan repaid out of a series A round after a year, and then gets that £13m equity pay-day in year five.

What a difference it makes not only to get your stake monies back, but also get them back early: a 67% annual compound return is boosted to nearly 90%.

Of course, this analysis assumes that the investor managed to negotiate a loan structure without any give-up on equity percentage. We’ll come back to that point later.

So, what’s not to like about loan structures?